Should you buy or rent your home?

Disclaimer: This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal, financial, or accounting advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any real estate transaction.

The first step towards getting somewhere is to decide that you are not going to stay where you are.

– J. P. Morgan

Should you rent or own where you live? This is a natural question many prospective first-time home buyers ask themselves. In this brief write up, we explore this question in the context of the Greater Seattle Area and lay out a data-driven and factual framework as to why we believe home ownership is the right approach if you value wealth creation.

First, to better understand the broader context of home ownership, I’ll provide a quick overview of the residential real estate market in Washington State. Then I’ll walk you through the three key drivers of wealth creation through home ownership followed by a few tactical moves to accelerate your growth.

Market overview

Why has home ownership served tens of millions of people in the US as a wealth creation vehicle? Fundamentally, this is driven by supply and demand: as population grows, major urban hubs and their suburbs continue to attract more people. At the same time, available and buildable land in desirable locations diminishes over time. This dynamic drives the price of real estate assets up over time.

Before discussing the specifics of wealth creation through home ownership, it is helpful to understand the local market a little better. To put the supply and demand forces in context, let’s look at a few data points from the local market. The population of Washington State increased by 1M from 6.7M to 7.7M people over the past decade. 70% of this increase (i.e., 700,000) was due to the population growth of the Greater Seattle Area. And this population growth is not just any population growth: Let’s go a little deeper by noting that about 10% of the population of the Greater Seattle area work in tech and that 62.6% of adults in the area are college graduates (#1 in the US). Despite the growing population, over the past decade, only 350,000 new housing units were built in Washington State. This persistent shortage of supply (which has been exacerbated by the increasing cost of development) combined with the growing pool of qualified buyers has manifested itself in the growing home prices.

Let’s consider the two cities of Bellevue and Lynnwood, both located in the Greater Seattle area. According to the Northwest Multiple Listing Service (NWMLS), the price of a typical home in Bellevue has increased by 227% from $535K to over $1.75M over the past decade (i.e., an annual growth rate of 12.5%). Over the same time period, a typical home’s value in Lynnwood has grown from $260K to $775K – an increase of 198%, which is equivalent to an annual increase of 11.5% (Figure 1). While price points in Bellevue and Lynnwood are quite different, the growth rates are similar. As a point of reference, over the past decade, the value of a typical US home has increased by 96% from $163K to $320K, which translates into an annual growth rate of only 7%.

Figure 1 Median home sales price in the decade leading to May 2022 (source: NWMLS)

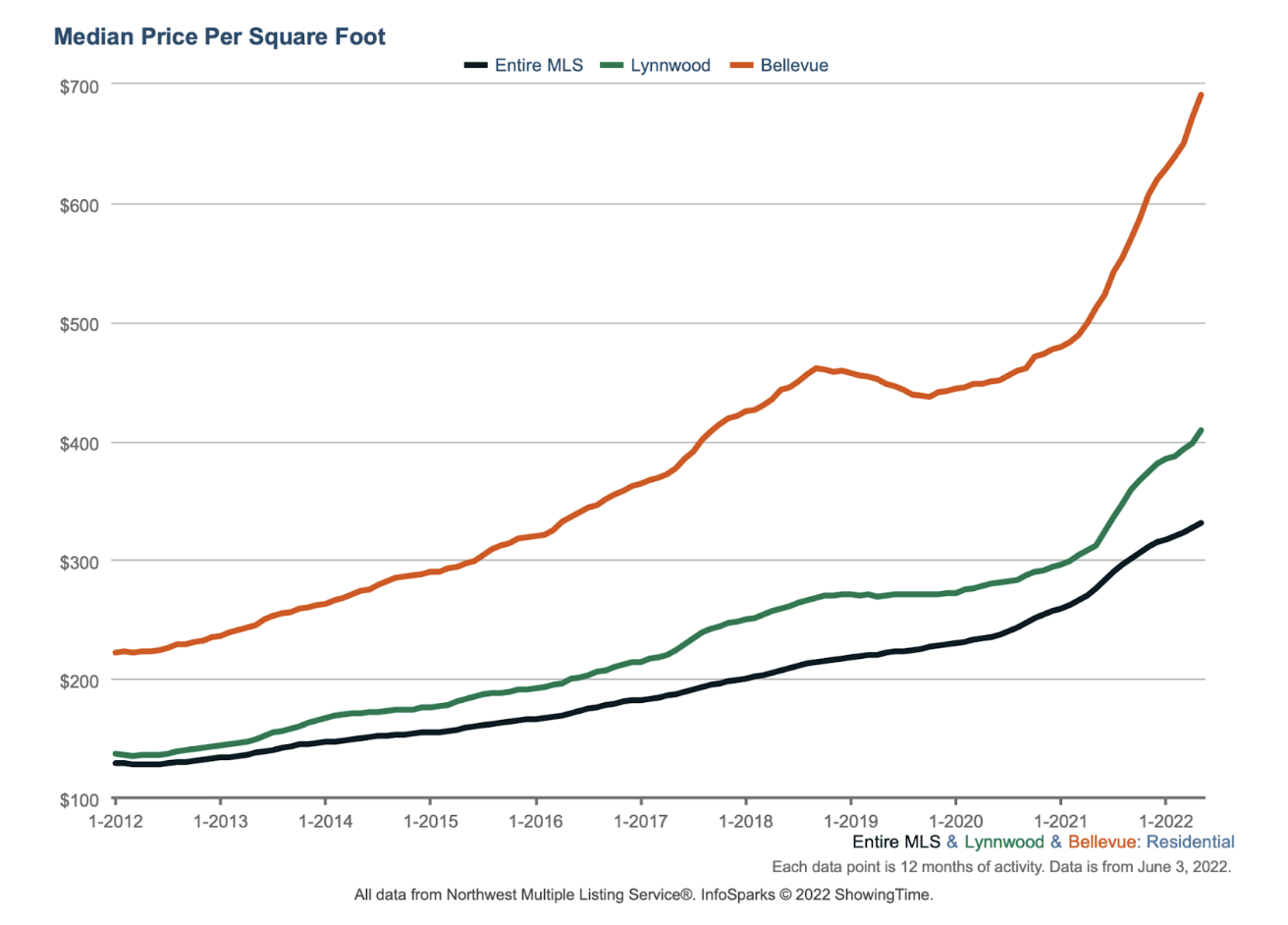

The upward price trend is similar if we look at the price per square foot in these areas (Figure 2).

Figure 2 Median home price per square foot in the decade leading to May 2022 (source: NWMLS)

Let’s look at the local real estate market growth from another perspective by considering days on market, which measures how long it takes to sell a home. Over the past decade, the median days on market for residential properties has been pushed down by a factor of 10, demonstrating an increasing supply shortage (see Figure 3).

Figure 3 Median home days on market over the decade leading to May 2022 (source: NWMLS)

Looking forward, while the local real estate market can experience short-term downturns, its strong performance is expected to continue in the long run because of the fundamental supply and demand forces, namely, a world-class local job market bringing in new population (both nationally and internationally) as well as a diminishing supply of buildable land combined with an increasing cost of development.

One last note on the market. As of early 2022, there are market signals pointing to potentially higher inflation rates in the coming years. In contrast to certain asset categories that may not perform very well in a high-inflation environment (e.g., tech stocks), real estate has historically done well as an inflation hedge.

What we outlined in this section sheds some light on why home prices in the area follow a strong upward trend. However, when you buy a home, price appreciation is only one of the contributing factors to your wealth. So taking a step back, the question is how exactly buying a home can create wealth for you. The next section answers this question.

The three wealth creation drivers in home ownership

Next we will look at the three key drivers of wealth creation through home ownership, which act in distinct, simultaneous, and harmonious ways: appreciation, tax benefits, and debt pay-off.

Wealth creation driver 1: Appreciation

The market overview presented in the previous section indicates why homeowners tend to do well: an increase in the market value of a rental property directly translates into an increase in the net worth of the owner. While it sounds intuitive, let’s dig a little deeper.

As a simplified example, suppose you buy a property in 2022 for $1M using a conventional mortgage with a 20% down payment. Assuming an annual growth rate of 8% (which is quite modest with the past decade in mind) the property will be worth about $1.36M in 2026. Now what would that mean to you as a home buyer:

Your net worth has increased by $360K. This is because once you buy a property, every dollar of market value appreciation of the property adds to your equity while having no effect on your loan balance. You owe the lender only the remaining loan balance regardless of the appreciation (in this example, your loan balance in 2026 will be the initial $800K less any principal paid off by 2026).

Of course, a $360K increase in net worth is nice, but as an owner, you also want to know what your return on investment (ROI) through appreciation is. While your property’s value has increased by an annual rate of 8%, that is not your ROI via appreciation. Your equity has gone from $200K in 2022 to $560K in 2026, which means your annualized ROI is 29%.

Why has your home increased in value by only 8% per year but your annualized ROI through appreciation is 29%? That is the power of leverage, which means buying assets using loans. Leverage is a common tool in the toolbox of wealthy individuals and prosperous businesses. (Note that if you bought the same property using all cash in 2022, while appreciation would still increase your net worth by $360K, your annual ROI due to appreciation would be only 8%.)

Wealth creation driver 2: Tax benefits

W-2 jobs and real estate involve different tax treatments. While taxation is too complex to fully explore here, let’s have a quick overview of four key tax advantages of owning your home:

Tax deductions: The following items are some of the deductibles for your home (subject to applicable rules and limits):

Mortgage interest

Property taxes

Mortgage points

Homeowners capital gain tax exemption: If/when you decide to sell your home, similar to any capital asset, the transaction will involve capital gain tax liability. The good news is that if you have lived there for at least two years in the past five year, you’ll be able to sell it while enjoying a tax exemption on up to $250,000 (if you’re single) or $500,000 (if you’re married) of your capital gain.

Adjusted basis: What does basis mean? Basis is the amount your home is worth for tax purposes. When you sell your home, it is quite possible that even after taking advantage of the above capital gain exemption to its maximum limit, you still have a capital gain obligation (meaning if you’re single and your capital gain is greater than $250,000, or if you’re married and your capital gain is greater than $500,000). That’s where the idea of adjusted basis helps. Any home improvements you might have made during the course of your home ownership (such as adding a bathroom or remodeling the kitchen) will be added to the initial basis, which is the cost to acquire the property, to arrive at an adjusted basis. In effect, all that means is that your home improvements are treated in the same manner as the cost to acquire the property, and therefore, reduce your capital gain tax obligation. (Note that there are other types of expenses that work in the same way but we won’t mention them here for brevity).

Exemption from the new Washington State capital gain tax: The 2021 Washington State Legislature recently passed a law which creates a 7% tax on the sale or exchange of long-term capital assets (stocks, bonds, business interests, and many tangible assets) when the gain is $250,000 or more. Note that this new tax law is currently being contested in the Washington Supreme Court. Regardless of the outcome of the contest and fortunately for home owners and real estate investors, real estate is exempted from this tax.

Wealth creation driver 3: Debt pay-off

When you pay rent, the money is gone. Unfortunately, there is not any proof of wealth for all the rent you’ve paid in the past. In contrast, when you own your home, as you gradually pay off the principal portion of your mortgage, your loan balance diminishes. This means your equity in the property gradually goes up by the same amount.

Wealth maximization tactics

In addition to the above key wealth creation drivers that work for you to increase your wealth, here we will look at a few tactical tools you can optionally leverage to further accelerate your wealth growth.

Rehab: When you rehabilitate a home, there are two positive outcome:

Forced appreciation. Instead of solely relying on the market to raise the value of your property over time, here you are pushing up the value of the property in a short period of time (e.g., through a 3-month rehab project).

Forced rent increase. Instead of just waiting for the market to increase the monthly rent, you can increase the rental cash flow by occasionally rehabilitating the property.

The key to a successful rehab project is targeted improvements. This means you need to be selective about which parts of the property to improve and which parts to leave alone in order to maximize your return. While rehab is an extensive topic, generally speaking, targeted cosmetic improvements as well as improvements involving adding square footage and adding bedrooms and/or bathrooms tend to yield the highest return.

Refinance: When you refinance a property, you replace the old loan with a new one. There are at least three reasons to consider refinancing a rental property:

Taking advantage of lower interest rates: If the current market interest rates are significantly lower than your loan’s interest rate, it might make sense to refinance in order to lower your monthly mortgage payments despite the closing costs of the new loan.

Increasing your return on equity (ROE) through cash-out refinancing: Suppose at some point down the road your equity in your home reaches 75%. While having a high equity in your home contributes to your net worth, it might not be the most productive use of your capital. A cash out refinance allows you to pull out a percentage of your equity in the form of a loan and put it to whatever use you see fit (e.g., as the down payment to acquire an investment property). Many lenders require the owner to maintain a minimum of 20% equity. So in the above example, you’d be able to pull out the equivalent of 55% of the appraised value of the home (e.g., $550K if your home is appraised at $1M).

Common questions first time home buyers ask

Before wrapping up, we’d like to highlight a few things that we have found important:

Home ownership sounds great, but what about the down payment?

In a high-price market such as the Greater Seattle Area, the down payment can be a barrier to first-time home ownership. While putting 20% down is a common choice, it is by no means the only option. There are a variety of options to buy your home with very little down payment — just ask us about down payment resources.

Should I wait until I can afford to buy my dream home?

Absolutely not. From a wealth creation perspective, the main point of buying your first home as soon as possible is to stop the financial bleeding due to your rent payments and start building wealth. Once you own a home, it is quite likely that after a while your personal, professional, and financial circumstances change and, as a result, you’ll be looking to buy a bigger and nicer house. At that point, you will have a couple of options: (1) Sell your first home given the tax advantages outlined earlier in the write up, or (2) Rent out your first home. Option 2 is the way many real estate investors started their real estate investment journey.

Your next step

If you’ve read this far, you have the desire to financially thrive. We hope this short write up helped you learn something new and concrete about wealth creation through home ownership. We’d love to speak with you about your real estate goals, put together a customized analysis of renting vs. buying for you, share our past results, and guide you in your wealth creation journey as your real estate broker and advisor.